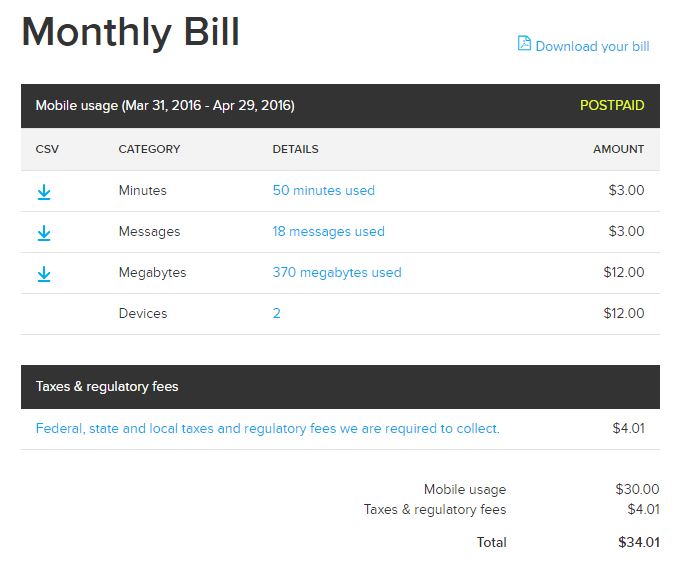

The verdict is officially in, and just as we suspected, we’re saving a ton of money after switching our wireless carrier to Ting. Our first bill, including taxes & fees, was $34.01, which breaks down as follows:

What a difference compared to the $135.70 we were paying to AT&T monthly. Plus this first bill was covered by the credits we received so we didn’t have to pay anything. Why oh why didn’t we switch sooner?

Full disclosure: I don’t think our monthly bill will be quite this low moving forward because we were trying to see how much we could lower it so we were a bit restrictive in our overall usage. That being said, we do have certain habits that keeps our usage naturally low.

Minutes

Who uses their phone to make calls? But seriously, we don’t talk on the phone much, and I’ve been using our MagicJack service via the iPhone app for long conversations with my family since we’re already paying a set amount for that service. No need to jack up our wireless bill unnecessarily.

Messages

Our AT&T plan restricted us to 200 texts per month or we’d pay extra per text, so for years we’ve been using an app called eBuddy XMS to communicate with each other and Facebook Messenger and Google Hangouts to “text” with friends and family.

Megabytes

I was grandfathered into an unlimited plan with AT&T so I never bothered connecting to Wi-Fi outside our home and consequently would use about 2 GB of data every month. One of the biggest changes I made after switching to Ting was taking advantage of free Wi-Fi networks when we’re out. I enjoy surfing when Joe is driving and I didn’t do much of that this first month either. Now that I know that it won’t impact our bill very much as long as I avoid the data hogging apps (I’m looking at you, Facebook), I’m going to be a little more relaxed about it.

Final Thoughts

I anticipate our Ting bill will be under $50 every month which is still an $80 savings over AT&T which is awesome.

How to switch to Ting

If you’re interested in switching to Ting, check out my post about our switch for full details, or check out my quick instructions below.

1) Open Ting account, order SIM card.

2) Request that your current carrier unlock your device.

3) After receiving your SIM card, log into your Ting account and choose activate.

4) Request through Ting that they port your number (optional).

5) Once port request goes through your old carrier will automatically cancel your account. Or if you’re not porting a number, call your carrier to cancel your service.

6) Install your Ting SIM card and follow your former carrier’s device unlock instructions.

7) If you have to pay an ETF, send that final bill to Ting and they will credit you back for a portion of it.

Enjoy the savings!